By Robert Laszewski

Rumors have been circulating in the marketplace all week that the administration was thinking of extending the individual health insurance policies that Obamacare was supposed to have cancelled for as much as three more years.

Rumors have been circulating in the marketplace all week that the administration was thinking of extending the individual health insurance policies that Obamacare was supposed to have cancelled for as much as three more years.

Those rumors have now come out into the open with Tom Murphy’s AP story on Friday.

That the administration might extend these polices shouldn’t come as a shock. My sense has always been that at least 80% of the pre-Obamacare policies would ultimately have to be canceled because of the administration’s stringent grandfathering rules that forced almost all of the old individual market into the new Obamacare risk pool.

But with the literal drop dead date for these old policies hitting by December 31, 2014, that would have meant those final cancellation letters would have had to go out about election day 2014. That would have meant that the administration was going to have to live through the cancelled policy nightmare all over again––but this time on election day.

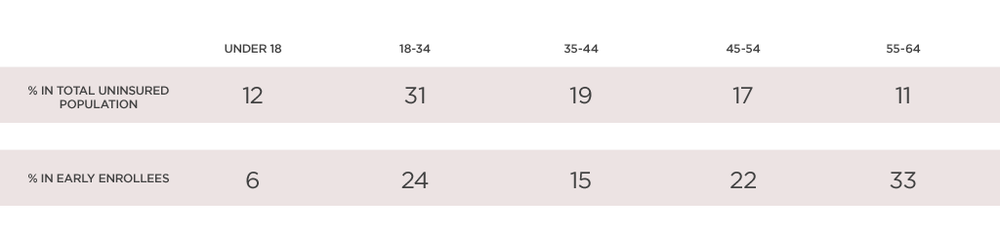

The health insurance plans hate the idea of another three-year reprieve. They have been counting on the relatively healthy block of prior business pouring into the new Obamacare exchanges to help stabilize the rates as lots of previously uninsured and sicker people come flooding in.

With enrollment of the previously uninsured running so badly thus far, getting this relatively healthier block in the new risk pool is all the more important. The administration’s now doing this wouldn’t just be changing the rules; it would be changing the whole game.

Republicans, and a few vulnerable Democrats, had essentially called for this last fall when legislation was floated in both the House and Senate with the “If You Like Your Policy You Can Keep It,” proposals. At the time, the administration and Democratic leaders rightly said if this sort of thing would have been made permanent it would have a very negative impact on what people in the new pool would pay––and on their already high deductibles and narrow networks.

At the beginning of this post I asked, Is Obamacare unraveling?

First, as I have said before on this blog, the law’s reinsurance provisions will mean Obamacare can keep limping along for at least three years. And, even making this change won’t alter my opinion on this. It will just cost the government more reinsurance money to keep the carriers whole.

By asking if it is unraveling, what I really wonder about is the whole sense of fairness in the law and the expectation that everybody needs to get the Democrat’s definition of “minimum benefits” whether they want them or not.

Continue reading…

When you are a patient at a hospital, you want to know that the executives who run that facility put the safety and quality of care above all other concerns. Encouragingly, more of them are saying that safety is indeed their number-one priority—a fitting answer given that preventable patient harm may claim more than 400,000 lives a year in the United States.

When you are a patient at a hospital, you want to know that the executives who run that facility put the safety and quality of care above all other concerns. Encouragingly, more of them are saying that safety is indeed their number-one priority—a fitting answer given that preventable patient harm may claim more than 400,000 lives a year in the United States.