By KIM BELLARD

I don’t really follow FinTech — I can’t even keep up with HealthTech! — but it caught my eye when Visa announced that it was acquiring FinTech company Plaid for $5.3b; a 2018 funding round valued the company at $2.65b. A 100% increase in valuation within a year suggests that something important is going on, or at least that people think something is.

I suspect there may be some lessons for healthcare in there somewhere.

For those of you who are equally as unfamiliar with FinTech’s terrain, Plaid has been described as the “plumbing” that supports many other FinTech companies. Launched in 2013, one in four people with a U.S. bank account are now believed to use Plaid to connect with 2,600 FinTech developers connected to more than 11,000 financial institutions. Its customers include Acorns, Betterment, Chime, Coinbase, Gemini, Robinhood, Transferwise, and Venmo. Plaid claims it connects with 200 million consumer accounts.

What terrifies Visa and rival Mastercard is that the future may be less card (credit/debit)-centric. In 2015, only 18% of internet-connected consumers worldwide had used a FinTech app to move money; in 2018 75% had. Plaid is one of the services that allow for such movement.

Rival Mastercard hasn’t been sitting idly; it had previously acquired FinTech companies VocaLink for $1b in 2016 and Nets for $3.2b in 2019, and had been an investor in Plaid. It has been trying to describe itself as a “multi-rails payment company.”

In a call with analysts, Visa CEO Al Kelly admitted:

We are increasingly trying to move from being strictly focused on payments, to being focused on the movement of funds for any purpose around the world. As big as Visa is in terms of the bank accounts that we can reach, we’re not as big as we need to be if we want to be a formidable player in money movement around the world.

Techcrunch says that what Plaid’s APIs do “is akin to what Stripe does for payments, but instead of facilitating payments, it helps developers share banking and other financial information more easily.” It adds that, with the acquisition, Visa “now has a view into scads of high-growth, private companies that are reinventing the world in which Visa operates. Buying Plaid is insurance against disruption for Visa, and also a way to know who to buy.”

CEO Mr. Kelly praised the acquisition, noting: “Plaid opens up new market opportunities by significantly expanding Visa’s network capabilities.” Mr. Kelly predicted that the acquisition would “expand a new financial data network” and add “new growth in core, as we work more closely with fintechs.”

Similarly, Visa President Ryan McInerney told Fortune: “Fintechs are clearly reshaping financial services, and Plaid is unquestionably the leader in this space…It’s something that positions Visa for the next decade and beyond.”

Meanwhile, healthcare struggles to share our data even between healthcare institutions using the same platforms, can’t seem to uniquely identify us, and is always trying to figure out who to chase for how much payment. It’s slow, inefficient, inaccurate, and very expensive.

There are companies like Noyo that are trying to change that. It describes itself as “modern architecture for health insurance,” and “the first API integration platform for health insurance.” Crunchbase even went so far as to say Noyo is “a sort of Plaid for health insurance data,” which Noyo liked so much that it quotes that description on its home page.

Founded in 2017 by veterans of troubled benefit software company Zenefits, Noyo has raised $4 million, and is still in the early stages of partnerships with carriers. Similar to Plaid’s strategy, Crunchbase said “Noyo wants its service to become a platform upon which other companies can build, but it doesn’t want to write all the apps.”

Healthcare doesn’t talk much about platforms, or at least it didn’t until the Mayo Clinic made a splash this past December by hiring the well-known health tech guru John Halamka, MD, as president of the Mayo Clinic Platform. Mayo describes its platform as “a strategic initiative to improve health care through insights and knowledge derived from data. The technology platform will elevate Mayo Clinic to a global leadership position within digital health care.”

Mayo just announced its first platform initiative, the Clinical Analytics Data Platform, “a strategic initiative to improve health care through insights and knowledge derived from data.” As part of the announcement, Dr.Halamka said:

Platform business models have been a force of disruption in many sectors, and the rapid digitalization of health care is affording us an unprecedented opportunity to solve complex medical problems and improve lives of people on a global scale

Mayo is certainly thinking globally, and it recognizes the opportunities that digital health affords, but I’m not sure that either it or the rest of healthcare see the threats, and opportunities, that platform models present. I’m not even sure that many in healthcare even understand what “platforms” in healthcare might look like, Noyo notwithstanding.

There certainly don’t seem to be many established healthcare companies that are as determined to be part of disruption in the same way that Visa and Mastercard are.

Credit/debit cards are well-entrenched in most consumers’ lives, especially in developed countries. Mastercard and Visa are huge, profitable, and seemingly indispensable. Despite that, FinTech solutions have sprung up to reach more consumers and reduce dependencies on networks like Visa and Mastercard. They’re not waiting to be toppled; they’re buying “insurance against disruption.”

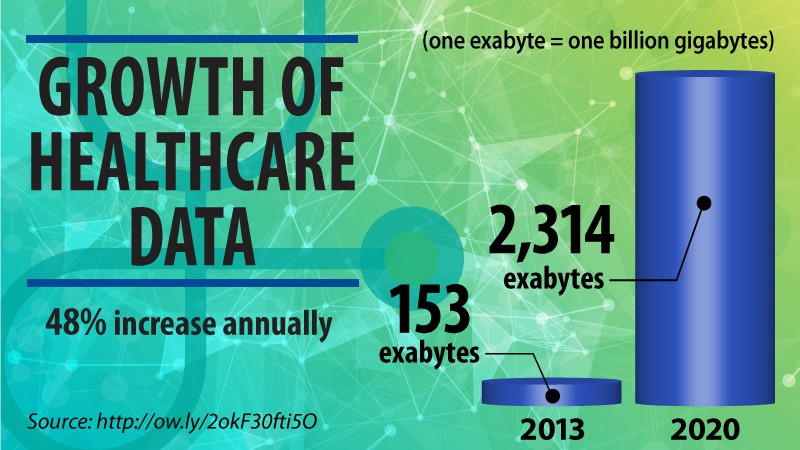

Healthcare has a data problem. It is too fragmented, too siloed, too complicated, and too difficult to use and to move. Its volume is growing exponentially, with more types coming from more sources. At the same time, more of the payment burden is falling directly on consumers, and they’re not happy about it.

In other words, it is ripe for disruption.

Disruption in healthcare won’t be easy, and it won’t come quickly. Then again, credit/debit cards aren’t going away anytime soon either, but Visa and Mastercard are preparing for a future in which they might, or at least in which their role is greatly diminished.

Healthcare organizations better start buying insurance for disruption that doesn’t look much like the current system. The platforms are coming.

Kim Bellard is editor of Tincture and thoughtfully challenges the status quo, with a constant focus on what would be best for people’s health.

Categories: Uncategorized

{kind=link}

{kind=link}

{kind=link}

“Mayo is certainly thinking globally, and it recognizes the opportunities that digital health affords, but I’m not sure that either it or the rest of healthcare see the threats, and opportunities, that platform models present. I’m not even sure that many in healthcare even understand what “platforms” in healthcare might look like…”

Right on target.

Healthcare hasn’t figured out how to tell patients what the price will be or what the surprise bill will look like, and we should be shocked that it hasn’t figured out how to use it’s own data.