Each week I’ve been adding a brief tidbits section to the THCB Reader, our weekly newsletter that summarizes the best of THCB that week (Sign up here!). Then I had the brainwave to add them to the blog. They’re short and usually not too sweet! –Matthew Holt

For today’s health care tidbits, there’s an old chestnut that I can’t seem to stay away from. I was triggered by three articles this week. Merril Goozner on GoozNews looked at the hospital building boom. Meanwhile perennial favorite Sutter Health and its price-making ability came up in a report showing that 11 of the 19 most expensive hospital markets were in N. Cal where it’s dominant. Finally the Gist newsletter pointed out that almost all the actual profits of the big health systems came from their investing activities rather than their operations.

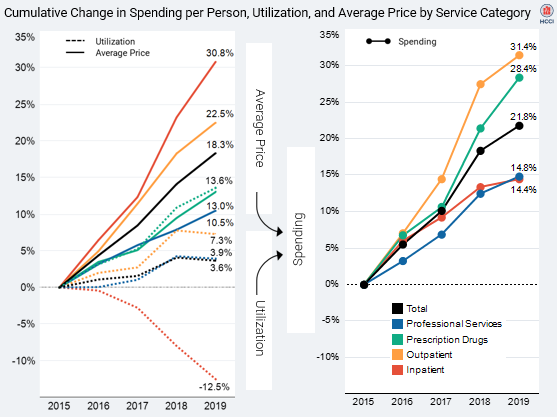

None of this is any great surprise. Over the past three decades, the big hospital systems have become more concentrated in their markets. They’ve acquired smaller community hospitals and, more importantly, feeder systems of primary care doctors. Meanwhile they’ve cut deals with and acquired specialty practices. For more than two decades now, owned-physicians have been the loss leader and hospitals have made money on their high cost inpatient services, and increasingly on what used to be inpatient services which are now delivered in outpatient settings at essentially inpatient rates. Prices, though, have not fallen – as the HCCI report shows.

The overall cost of care, now more and more delivered in these increasingly oligopolistic health systems, continues to increase. Consequently so do overall insurance premiums, costs for self insured employers and employees, and out of pocket costs. And as a by-product, the reserves of those health systems, invested like and by hedge funds, are increasing–enabling them to buy more feeder systems.

Wendell Potter, former Cigna PR guy and now overall heath insurer critic, wrote a piece this week on how much bigger and more concentrated the health plans have become in the last decade. But the bigger story is the growth of hospital systems, and their cost and clout. Dave Chase likes to say that America has gone to war for less than what hospitals have done to the American economy. That may be a tad hyperbolic, but no one would rationally design a health care environment where non-profit hospitals are getting bigger and richer, and don’t seem to be able to restrain any aspect of their growth.

Categories: Uncategorized

Hospital mergers including merging with independent free standing hospitals ,specialty practices and community hospitals should result in cost savings passed on to the patients, all while improving access to care. The truth lies in the data. Clinical outcomes data together with hospital benchmarking KPIs would highlight the success of the newly evolved health system post the merger.